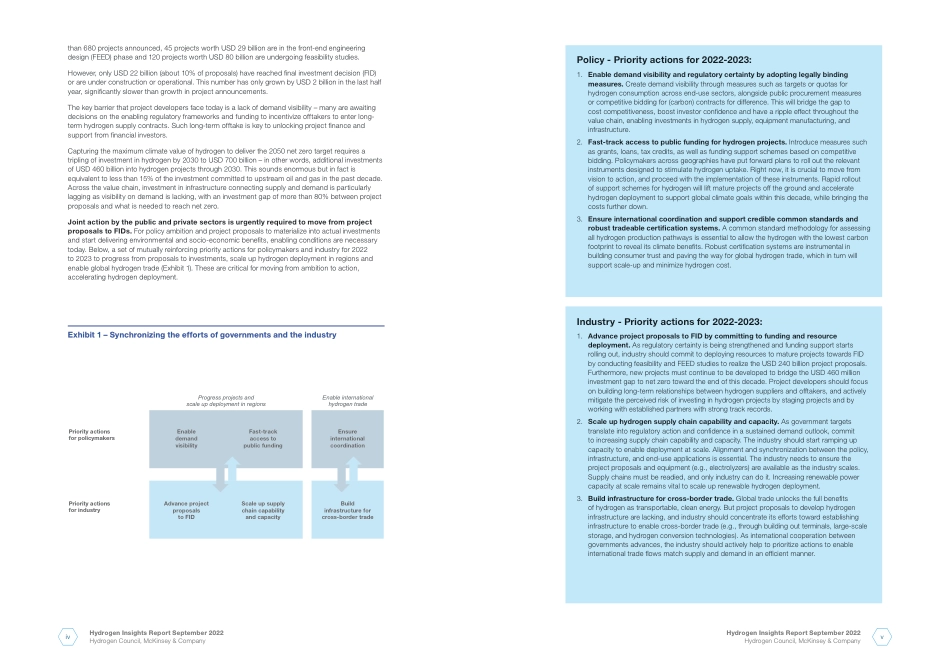

Hydrogen Insights 2022 An updated perspective on hydrogen market development and actions required to unlock hydrogen at scaleSeptember 2022Executive summaryThe pipeline of hydrogen projects is continuing to grow, but actual deployment is lagging. In 2022 some 680 large-scale hydrogen project proposals, equivalent to USD 240 billion in direct investment through 2030, have been put forward – an investment increase of 50% since November 2021. Yet, only about 10% (USD 22 billion) have reached final investment decision. Europe is home to over 30% of proposed hydrogen investment globally. However, other regions are leading the implementation on the ground: 80% of operational global low-carbon hydrogen production capacity is in North America, while China has surpassed Europe in electrolysis with 200 megawatts (MW) operational, versus 170 MW in Europe, driven by strong government support. South Korea and Japan, in turn, are leading on fuel cells, driven by strong government and corporate ambitions: more than half of the 11 gigawatts (GW) of global fuel cell manufacturing capacity is located there, and Japan has ramped up deployment of hydrogen-ready combined heat and power (CHP) plants, with 425,000 such systems installed.The urgency to invest in mature hydrogen projects today is greater than ever. The rebound of carbon emissions to above pre-COVID levels, the invasion of Ukraine, and the growing concerns around energy security resulting from the war in Europe make one thing clear: our economies need clean hydrogen, and action is needed to convert proposals into actual deployment. Out of the more The pipeline of hydrogen projects is continuing to grow, but actual deployment is lagging. 680 large-scale project pr...