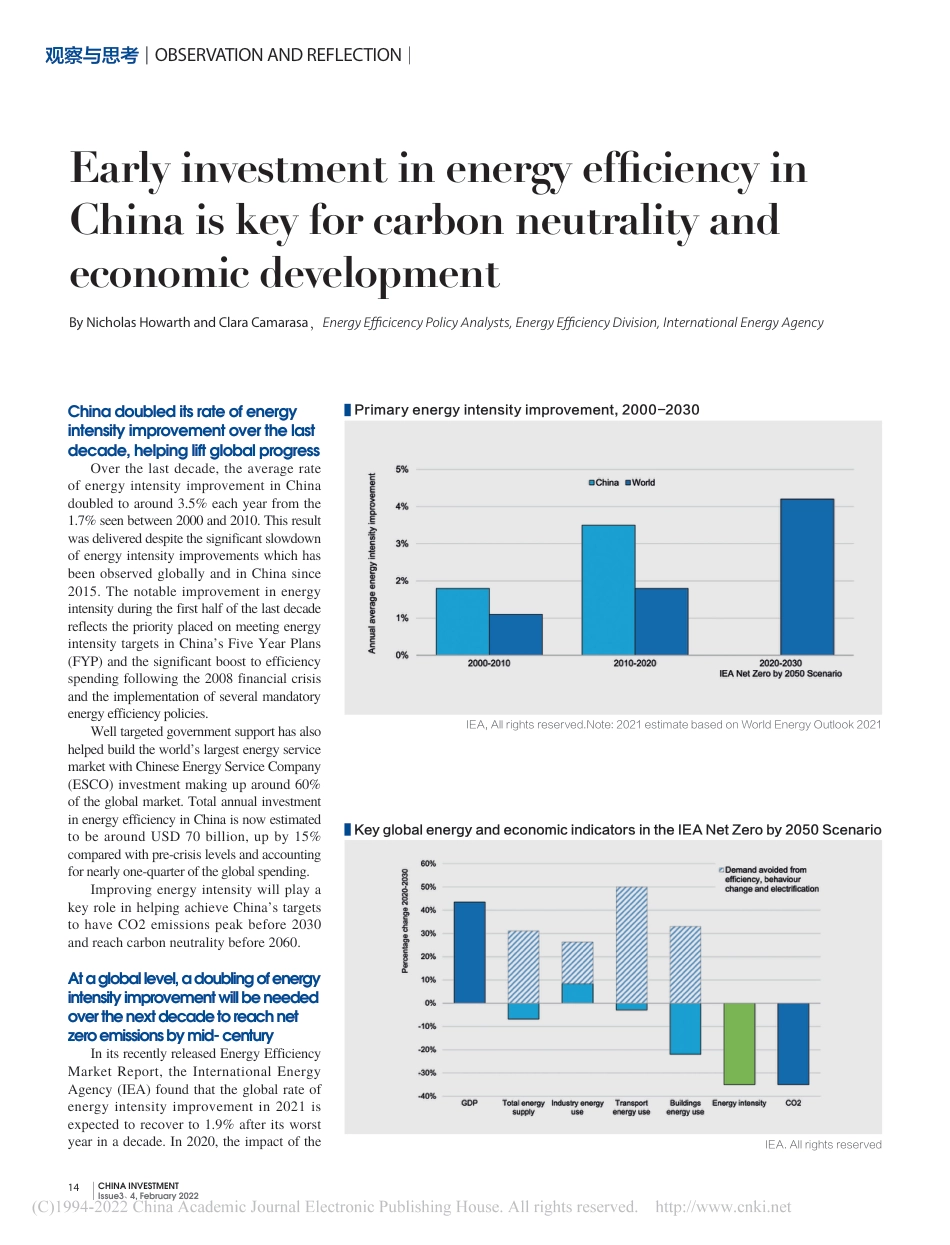

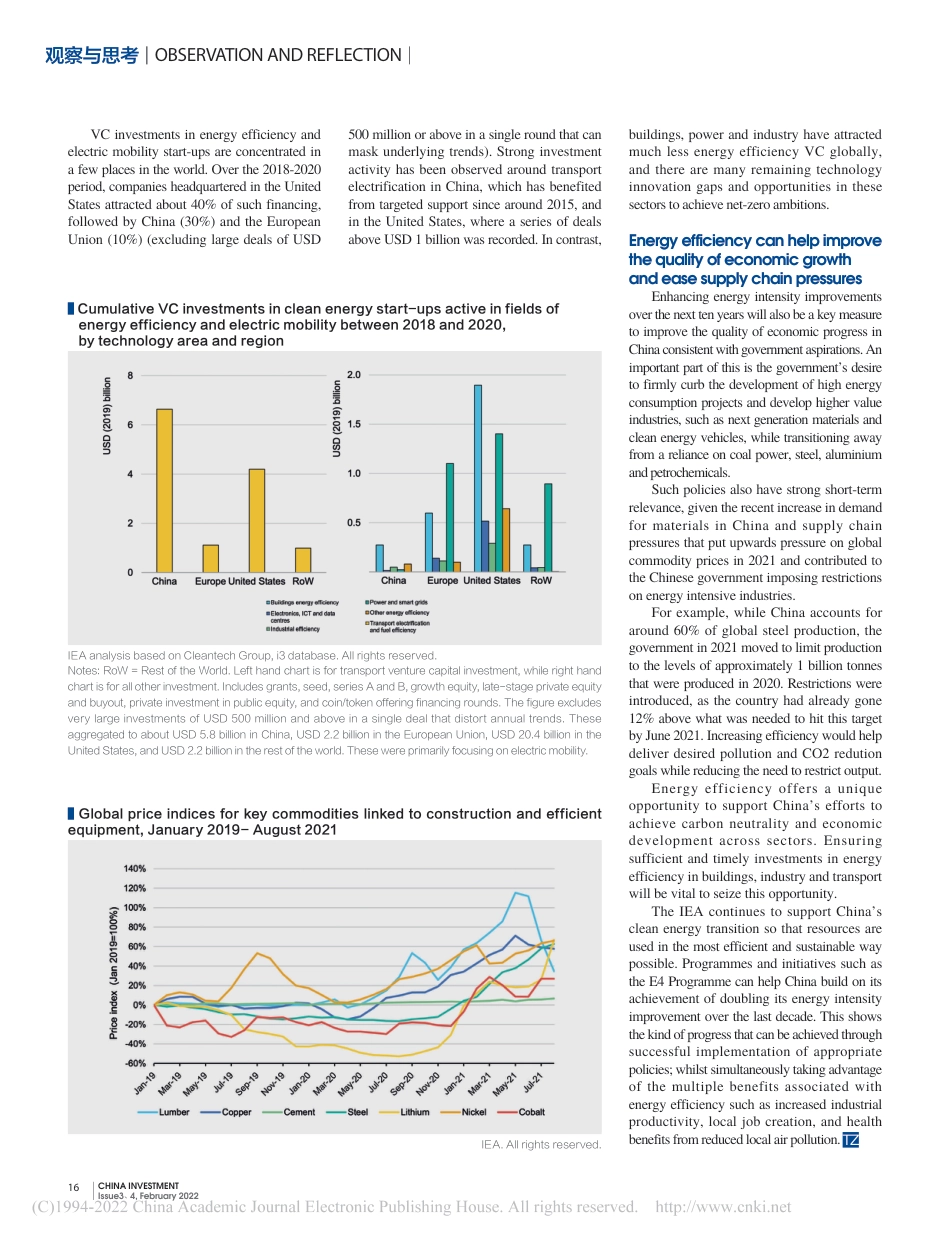

14CHINA INVESTMENTIssue3、4, February 2022By Nicholas Howarth and Clara Camarasa,Energy Efficicency Policy Analysts, Energy Efficiency Division, International Energy AgencyEarly investment in energy efficiency in China is key for carbon neutrality and economic developmentChina doubled its rate of energy intensity improvement over the last decade, helping lift global progressOver the last decade, the average rate of energy intensity improvement in China doubled to around 3.5% each year from the 1.7% seen between 2000 and 2010. This result was delivered despite the significant slowdown of energy intensity improvements which has been observed globally and in China since 2015. The notable improvement in energy intensity during the first half of the last decade reflects the priority placed on meeting energy intensity targets in China’s Five Year Plans (FYP) and the significant boost to efficiency spending following the 2008 financial crisis and the implementation of several mandatory energy efficiency policies.Well targeted government support has also helped build the world’s largest energy service market with Chinese Energy Service Company (ESCO) investment making up around 60% of the global market. Total annual investment in energy efficiency in China is now estimated to be around USD 70 billion, up by 15% compared with pre-crisis levels and accounting for nearly one-quarter of the global spending.Improving energy intensity will play a key role in helping achieve China’s targets to have CO2 emissions peak before 2030 and reach carbon neutrality before 2060.At a global level, a doubling of energy intensity improvement will be needed over the next decade to reach net zero emissions by mid- centuryIn its recently...