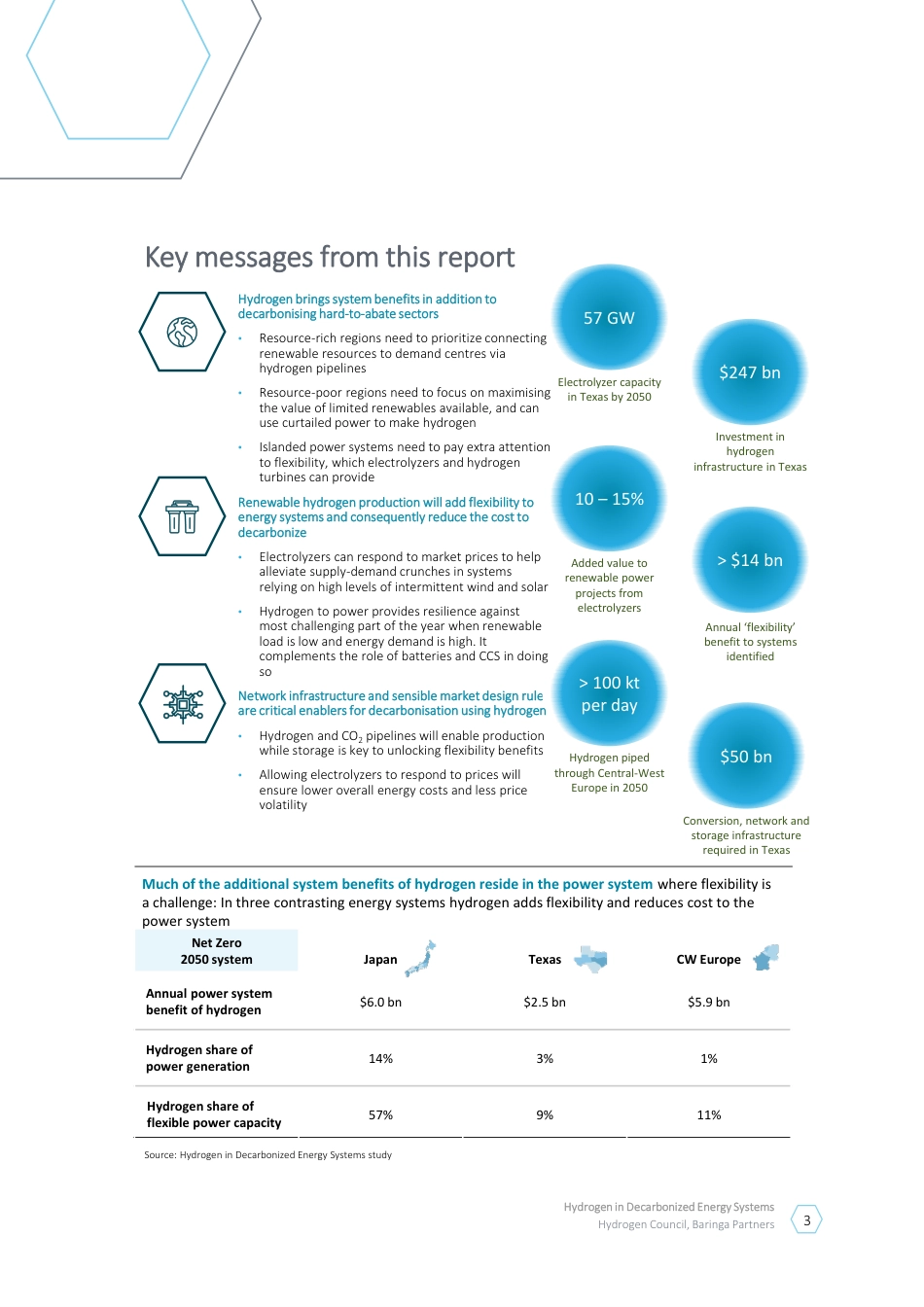

Hydrogen in Decarbonized Energy SystemsThis report was authored by the Hydrogen Council in collaboration with Baringa Partners LLP. The authors of the report confirm that:1. There are no recommendations and / or any measures and / or trajectories within the report that could be interpreted as standards or as any other form of (suggested) coordination between the participants of the study referred to within the report that would infringe the EU competition law; and2. It is not their intention that any such form of coordination will be adopted. Whilst the contents of the report and its abstract implications for the industry generally can be discussed once they have been prepared, individual strategies remain proprietary, confidential, and the responsibility of each participant. Participants are reminded that, as part of the invariable practice of the Hydrogen Council and the EU competition law obligations to which membership activities are subject, such strategic and confidential information must not be shared or coordinated – including as part of this report.2Hydrogen Council, Baringa PartnersHydrogen in Decarbonized Energy SystemsKey messages from this reportHydrogen brings system benefits in addition to decarbonising hard-to-abate sectors•Resource-rich regions need to prioritize connecting renewable resources to demand centres via hydrogen pipelines•Resource-poor regions need to focus on maximising the value of limited renewables available, and can use curtailed power to make hydrogen •Islanded power systems need to pay extra attention to flexibility, which electrolyzers and hydrogen turbines can provideRenewable hydrogen production will add flexibility to energy systems and consequently reduce the cost to decarbo...